Over the last three decades organic food and farming has been growing year by year across the EU and continues doing so. The EU’s organic market is very dynamic with growth rates varying between countries. Policies can positively impact this growth – both production and consumption.

In 2022, the EU’s total area of farmland under organic production grew to 16.9 million hectares. Compared to 2021, the number of organic producers in the EU increased by 10,8% to 419,112. However, the EU’s organic retail market does not accompany the significant production growth, decreasing by 3% as to 2021 data and resulting in 45.1 billion EUR, still the second largest market, after the USA and followed by China.

The EU’s organic market is very dynamic with growth rates varying between different countries. Its continuous positive development is due to a combination of factors. Besides the innovative character of organic food and farming, growing policy support and European citizens increasing demand for high-quality, sustainable food production, despite the geopolitical situation and the ongoing war in Ukraine. This is well represented in the growing per capita consumption of organic products, which reached 102 EUR on average. Generally speaking, consumers spend more on organic food every year with certain product groups achieving above-average market shares.

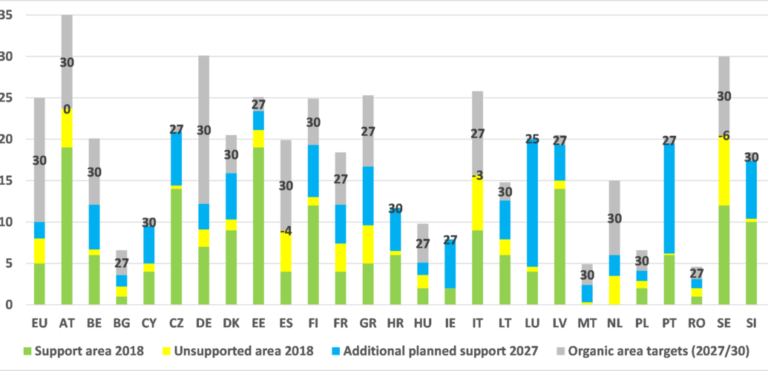

In May 2020, the European Commission’s Farm to Fork Strategy mentions organic as a key sector to achieve the European Green Deal’s food ambitions. The strategy states that “The market for organic food is set to continue growing and organic farming needs to be further promoted”. As part of this strategy, the Commission published the 2021-2027 Organic Action Plan, which aims at boosting both organic demand and supply. Measures of the Common Agricultural Policy (CAP) should also be paramount in in reaching “the objective of at least 25% of the EU’s agricultural land under organic farming by 2030 and a significant increase in organic aquaculture”, as laid out in the Farm to Fork Strategy.

It is crucial to link this target to the Common Agricultural Policy (CAP) reform, the Biodiversity Strategy and other agri-food policies to create a more positive environment in which farmers and food companies feel confident making significant investment decisions to meet consumers’ demand for products produced with a heart for people, animals and the planet. So far, we regret that the CAP reform did not sufficiently align with the target of 25% of organic land in the EU even if we welcome the introduction of national target of organic land to reach for Member States.

Browse production and market data

Do you want to know more about organic production and market data in Europe? Browse our interactive infographic. The infographic displays organic production and market for all EU Member states and European Free Trade Association (EFTA) countries. This year, we have also updated and added the statistics data on Ukrainian organic production and retail market.

https://www.organicseurope.bio/infovis/release/?2024

Background information

Since 2000, the Research Institute of Organic Agriculture (FiBL) compiles a yearly overview of the most recent data on organic production and retail in Europe and the world in “The World of Organic Agriculture: Statistics and Emerging Trends 2024”. Together with FiBL, we fit the European data in our interactive infographic.

Supported by

This infographic is supported by Green Organics, NaNa Bio, Rapunzel, the Mediterranean Agronomic Institute of Bari (CIHEAM Bari) and the Mediterranean Organic Agriculture Network (MOAN).

Directorate-General for Agriculture and Rural Development (DG AGRI) of the European Commission as well as the Ekhaga Foundation co-finance this publication.

Full article: https://www.organicseurope.bio/about-us/organic-in-europe